The Amazon Effect: Why B2B Payment Expectations Have Forever Changed

Think about the last time you ordered something online. With just a few taps, you confirmed your purchase, selected your preferred payment method...

Modernizing how you process B2B payments can help streamline your payment operations and strengthen vendor relationships. It allows you to process invoices 74% faster and lessen the workload for your accounts payable team.

But when it comes to B2B payments, there are plenty of alternatives out there — after all, it’s a global market valued at $120 trillion. Understanding how each method works and the differences between them will help you determine which one best fits your business.

But with so many different options available, where do you even start?

In this article, we’ll cover different B2B payment methods in depth, including the benefits and drawbacks of each. We’ll also look at how you can simplify the payment process for you and your suppliers with a payment automation solution.

Click the links below to jump ahead:

Business-to-business (B2B) payments are transactions that occur between two business entities for goods or services provided. Example entities can include manufacturers, wholesalers, distributors, and contractors.

Payments between two companies are typically made after an order is fulfilled — something known as billing in arrears.

Consider a restaurant that hires a commercial cleaning service. This B2B transaction is fairly straightforward. The cleaning company sends an invoice after delivering the services, and the restaurant pays it within an agreed timeframe.

Of course, this is just one example. Business transactions can become more nuanced depending on the goods or services required.

A business-to-consumer (B2C) transaction is when a consumer pays a company for goods or services, typically for personal use. Examples include shopping for new shoes or grabbing lunch with a friend. However, B2B payments aren’t as straightforward.

Let’s take a closer look at how B2B and B2C payments differ.

B2B payments are much larger in terms of the size and volume of the transactions.

A company might purchase tens of thousands of dollars worth of goods, whereas a consumer might only spend a hundred dollars on a shopping trip.You might expect B2C payments to be higher than B2B payments given their scale, but that’s not the case. The global B2B eCommerce market was valued at $14.9 trillion in 2020, which is over five times the B2C eCommerce market.

Companies order goods or services from other companies on a more frequent basis. For example, a grocery store will often have recurring orders from different distributors.

In contrast, B2C payments are generally one-time payments for personal use. Of course, there are some exceptions as consumers may order the same goods repeatedly over time.

Given the size of each transaction, payment terms are more complex for B2B transactions. There are also additional processes in place before any funds can be released.

Common terms for B2B transactions are net 30, net 60, and net 90, which indicates the number of days until payment is due. Some vendors may offer early payment discounts (e.g., 2/10 net 30 meaning that a 2% discount is applied if the invoice is paid within 10 days).

Terms for B2C payments are more straightforward. Payments are typically made before any goods or services are provided.

Finally, payment methods differ for B2B and B2C payments.

When paying for your morning coffee, you might use your debit or credit card. You might even use a digital wallet like Apple Pay or Google Pay if that option is available.

While B2C payments are made at the point of sale using cash or credit, payment methods for B2B transactions are typically different, relying on checks, wire transfers, and other options, which we’ll cover in more detail in the next section.

There are many different methods that companies use to receive and transmit payments for B2B transactions. Understanding how each works will help you determine which one is right for your business.

Let’s break down the six most popular B2B payment methods.

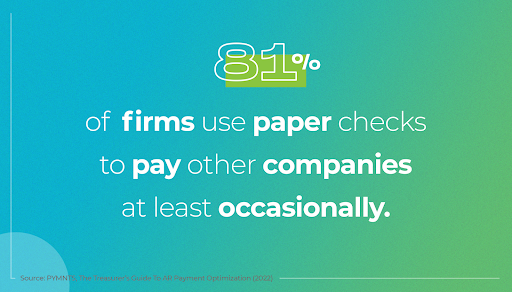

Paper checks may seem like an antiquated form of payment, but they’re still widely used for B2B transactions. In fact, 81% of companies still use paper checks to pay other businesses at least occasionally.

While paper checks are a familiar payment method, the drawback is that they take longer to process. It can take days or even weeks to receive and deposit a check.

Paper checks are also a major source of fraud as they lack the security measures of more secure payment methods. In fact, paper checks account for 66% of fraud activity.

Companies can use credit cards to make B2B payments and manage part of their cash flow. They can charge purchases on a card and pay off the balance before any interest is due.

While credit cards offer a secure way of making and receiving payments, they incur fees of 1.5% to 3.5% for each B2B transaction. When you’re processing a high volume of invoices, fees from credit card payments can quickly add up.

Companies may also use virtual cards to make online B2B payments. These are 16-digit bank card numbers that are generated for each transaction and intended for one-time use only.

What’s more, you can designate specific amounts and vendors for each virtual card. This provides an extra layer of security as each card can’t be processed for more. It also prevents bad actors from processing the transaction.

ACH payments are electronic bank-to-bank payments that are conducted via the Automated Clearing House network, which is run by the National Automated Clearing House Association (NACHA).

ACH transfers typically have the lowest processing fees. Some payment providers charge a flat rate of $0.20 to $1.50 per transaction, while others allow you to make ACH transfers without paying any fees.

Standard ACH transfers take three to four business days to process. However, businesses can also opt for Same Day ACH transfers. Transfer limits for Same Day ACH transfers were raised from $100,000 to $1 million.

Wire transfers are secure payments between financial institutions. Domestic wire transfers can take less than 24 hours, while international payments can take up to five days to complete.

Costs for wire transfers depend on the financial institution you’re using and whether you’re sending or receiving a domestic or international transfer.

Here are median wire transfer fees for 11 different banks:

Finally, gateways like PayPal, Square, and Stripe enable businesses to accept and make payments for goods or services online during the checkout process. A payment gateway makes it easy to make or receive recurring payments (common for subscription services) as well as one-time payments.

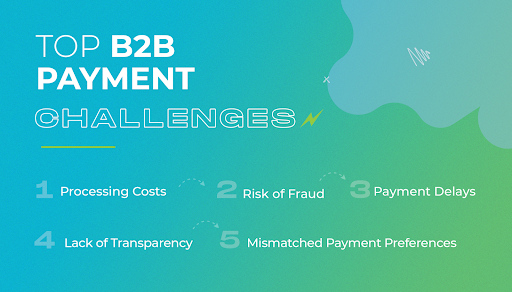

B2B payments are complex and present numerous challenges for companies of all sizes. It’s important to consider these when choosing a payment method for your business.

Here are some of the many challenges associated with B2B payments.

Transaction fees differ for each B2B payment method. While wire transfers and credit cards may offer a convenient way to accept payments, they also tend to incur higher fees. These fees ultimately lower your profit margins.

The risk of fraud is an important concern when it comes to issuing payments. Nearly 75% of organizations were targets of payment fraud attacks in 2020.

In addition to matching invoices against purchase orders and goods receipt notes (known as a three-way matching), using secure methods to issue payments can help reduce the risk of fraud.

Payment delays can make it difficult for your company to manage its cash flow. One study found that 57% of B2B payments for small to midsize businesses were collected late.

However, payment delays can also stem from slow invoicing processes and manual payment methods (it takes longer to process a check than an electronic payment).

Transparency into processes like invoicing is crucial for managing your cash flow and avoiding late payments. However, tracking the status of individual payments can be difficult for payment methods like cash, checks, and money orders.

Another challenge with making and accepting B2B payments is mismatched payment preferences — some vendors may only issue checks, while others may prefer ACH.

Payors often don’t match payees’ preferences because of poor communication or because they don’t have the right technology. Handling vendor enrollment through a portal can help your company address mismatched payment preferences.

B2B payment challenges are different for every company. By adopting a modern payment automation solution like DocuPhase, you can:

B2B payment methods differ in ease of use, cost, speed, and security. Which one you choose to process payments will depend on various factors.

With that said, more businesses are moving away from manual payment methods like paper checks toward electronic and digital payments. They’re also turning to payment automation solutions to manage and process invoices.

If you’re looking to streamline your B2B payment operations, then request a demo today to see how our solution can transform how you accept and transmit payments.

Think about the last time you ordered something online. With just a few taps, you confirmed your purchase, selected your preferred payment method...

There are a lot of misconceptions about virtual cards that prevent companies from adopting and taking advantage of their varied benefits. Virtual...

Manufacturers have poured resources into AI, IoT, and automation to improve production, and it’s paying off. Factory floors are more efficient than...